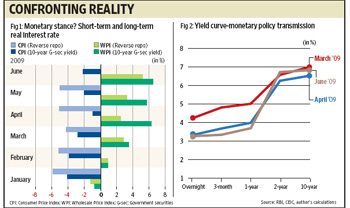

The first chart illustrates the monetary policy conundrum of divergent signals on inflation. Real interest rates show that monetary policy is still too tight using Wholesale Price Inflation WPI (right of the plot), and too lax using Consumer Price Inflation (CPI). How should the RBI read interest rates in assessing the stance of monetary policy?

The second chart underscores that different interest rates can move very differently in India, unlike advanced countries where there is a smooth transmission mechanism across the yield curve. In response to a 25 basis points (bps) reduction in policy rates in April, the yield curve shifted downwards at the short end, but remains stubbornly elevated at the long end.

So, as the governor implied, much depends upon which inflation measure and interest rate you are examining and why you need to push the limits of monetary policy beyond setting interest rates to make it effective.

As it reviews its monetary stance, the RBI must delve beneath the aggregates to balance its goal for output stabilization with that for inflation. For even as all indications suggest a pause on interest rates, the central bank must anchor inflationary expectations beginning to get unhinged and maintain a low-interest rate environment to facilitate output recovery.

An accommodative monetary stance is doubtless needed to maximize gains from an expansionary fiscal policy in order to support growth, nascent signs of which are emerging in some sectors. Output recovery, however, has not yet stabilized forcefully: While manufacturing output rose 2.5 per cent year-on-year (y-o-y) in May and consumption growth turned positive, the contraction in capital goods accelerated too. The growth of monetary and other aggregates has yet to pick up: While broad money growth at 21 per cent (y-o-y) since April is above projection, non-food credit growth is substantially below trend—averaging 16 per cent annually in April-June, with annualized, seasonally-adjusted monthly momentum also averaging 13.7 per cent. So, it is critical to sustain revival in consumption and set the stage for a recovery of the investment cycle, which typically lags behind consumption.

Is there scope for further interest rate cuts? Using the Taylor rule — the RBI doesn’t really use it, but it is a useful rough guide nevertheless— the short-term nominal interest rates ought to be 0.2 per cent by WPI and 13.3 per cent by CPI (assuming a negative output gap of 0.4 per cent, a 3 per cent equilibrium real rate of interest and a 4 per cent inflation target). With past volatility distorting the inflation rate, the gross domestic product (GDP) deflator (2.2 per cent, January-March) is possibly a more accurate reflection of price changes at this juncture — this suggests a nominal interest rate of 4.1 per cent — close to the actual policy rates. Quite possibly, the RBI is with the curve or, perhaps, even ahead of it.

Two reasons, however, weaken the case for further reduction in interest rates.

One, inflationary expectations have not been adjusting to the decline in inflation—CPI is lagging and is still above 8 per cent, indicating that second-round effects are yet to reverse. Plus, sequential inflationary momentum, seasonally adjusted, has been rising since April. Some core prices are accelerating and food price inflation is persistent at both producer and retail levels. Add to these the possible inflationary threat from a monetary overhang in the medium term. Market expectations of rate increases from September have been rising, with several banks expecting a reversal of the monetary easing. Resurgence of inflationary pressures, therefore, poses a significant upside risk in the near term, forcing the RBI’s attention towards the price stability objective.

Two, there is little to be gained from interest rate cuts, for which a modest 25 bps scope might exist, at this point. The gap between the short-term and long-term nominal rates stood at 358 bps in June, widening from 134 bps in March, while policy rates moved further down. This is already undermining policy credibility and the RBI would look silly reducing interest rates with market-based indicators veering in another direction. The truncated transmission of previous interest rate cuts is an outcome of several factors: large government borrowings, increasing risk aversion by banks, growing uncertainty about inflation and long-term interest rates among investors, etc.

The challenges before the monetary policy review, therefore, are that inflationary expectations are well anchored and long-term interest rates do not rise too much. But the RBI has to do this without resorting to the interest rate tool.

It has already acted on the latter front with the revised government borrowing schedule and supportive open market operations, to which the bond market has responded positively. Surplus funds with banks, due to buoyant deposit growth at an annual average of 22 per cent since April, far exceed the growth in non-food credit currently and support the RBI’s efforts, as do the surplus liquidity adjustment facility balances, averaging Rs1.2 trillion daily. The RBI will thus flag the positives to assure markets of continued efforts at maintaining abundant liquidity to prevent any large spike in bond yields.

It will also reiterate its firm commitment to keep inflation under check. Price stability may, thus, move more centre stage alongside growth, compared with the previous announcement, to anchor inflationary expectations. Will it announce its inflation projections for the year? It mentioned an inflation rate of 4 per cent at end-March 2010 in April, but omitted a target — expressing commitment to a tolerance zone for inflation at this point may be another way to anchor expectations. Finally, an exit strategy from the unprecedented measures taken in the wake of the global financial crisis might also signal an impending shift.

This article originally appeared here in Mint.

Renu Kohli is a New Delhi based economist. She is formerly with the Reserve Bank of India (RBI) and the International Monetary Fund (IMF).